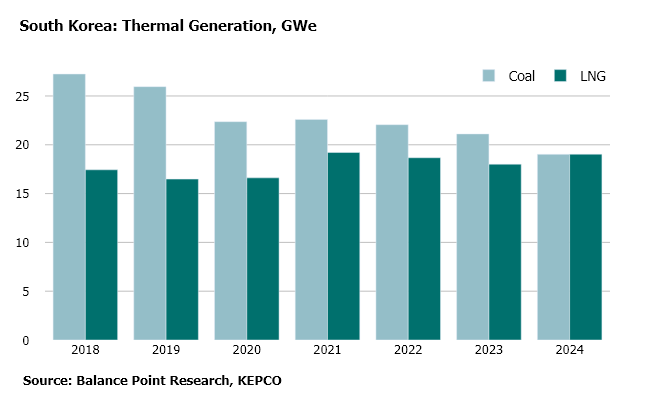

South Korea: Power generation from LNG imports ties coal for the first time

For the first time in 2024, the amount of power generation that South Korea’s power market sourced from LNG was equivalent to coal on an annual basis. The decline in coal generation, which until 2024 was also the South Korean market’s single largest source of generation, has been particularly remarkable in that it has not enabled significant LNG demand growth.

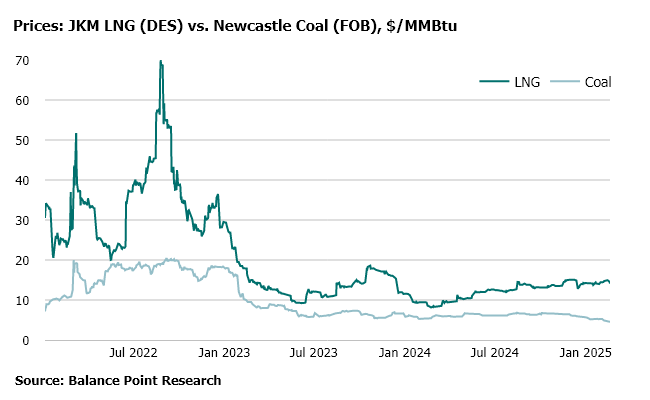

Rather, coal’s decline has allowed power generation associated with LNG imports to remain resilient in a period when a.) South Korea’s volume of generation from nuclear and renewables increased and b.) global gas flat prices traded at historic levels as illustrated in the graph further below. In large part, the dynamics at play in South Korea’s power sector also explain the static nature of the market’s LNG imports, which have been stuck at 46 Mtpa (equivalent to 63 BCM, or 6.1 bcfd) in recent years.

Going forward, the fate of the remainder of South Korea’s still sizeable stack of coal generation will depend on an array of factors.

In recent years, prioritization of the clean-air measures by South Korea’s domestic political process has resulted in small reductions in the cost competitiveness of coal generation. For example, starting in 2022, coal generators have been required to include a limited amount of carbon cost in their dispatch offers to South Korea’s electricity market operator. There are nevertheless several challenges to the further integration of emissions cost into the economics of generating power in South Korea. An important one is a great political sensitivity to passing through the added costs of emissions to end users. Looking forward, South Korean domestic politics could travel in a variety of directions, which encourage either a further decline or even a revival in the level of coal generation.

Further on the topic of the cost of generation, but external to South Korea, is the potential for changes in the global gas market that reposition the competitiveness of JKM-indexed gas generation. In the shorter-term, the gap between spot LNG and coal is widening. But in the not too distant future, it is not unimaginable that shifts in global energy markets could more competitively position the economics of gas and coal generation in South Korea.