India: Power load sets records. Will coal keep pace?

Since October 2024, Indian power load has averaged +7 GWe year-on-year growth. Strong economic conditions and warm temperatures have propelled the market’s demand for power.

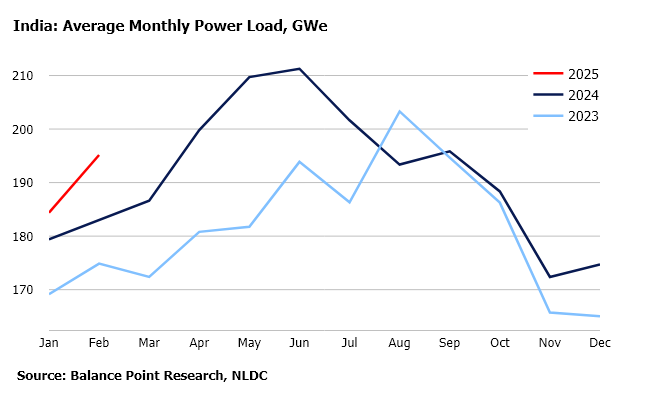

For the quarter ending in December 2024, India’s real GDP growth rate improved to +6.2% compared to the softer +5.6% growth achieved during the prior quarter. Although January and February are typically India’s coolest months, temperatures in 2025 have been warmer than average. In Mumbai, cooling degree days (CDDs) in January 2025 and February 2025 were approximately double their levels for the year prior.

As India heads into the heat of the pre-Monsoon season during the coming months, those interested in global LNG balances should question how India’s power market will balance. The topic is especially relevant at the conclusion of a week of gas trading in Europe during which TTF front month prices briefly declined to close to 41 Euros.

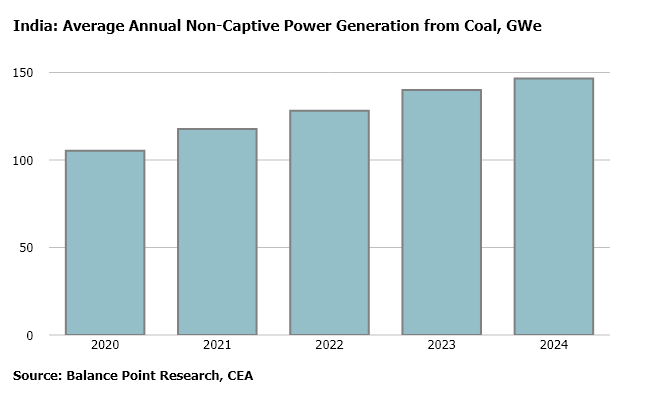

Historically, coal generation has anchored the development of India’s power market. While generation from coal continued to grow on an annual basis in 2024, it was nonetheless challenged to address the magnitude of power load growth that occurred from April 2024 to June 2024.

February 2025’s outturn for coal generation was a mere 5 GWe from coal’s monthly peak in 2024. If India’s economy and climate continue to run warm during the months ahead, the market’s bid for generation from natural gas and LNG imports should see further commercial momentum.