Algeria: Steady underperformance

If the marketing of Algeria’s natural gas exports were compared to a car, a smaller model by Nissan with under-powered acceleration at higher gears might be an appropriate comparison. Similar to sedans produced by Nissan, the heyday for Algerian gas exports was arguably pre-2010. Today, by contrast, natural gas export flows from Algeria materially underperform its existing midstream capacity both in terms of pipeline capacity to Europe and liquefaction capacity to the global market. In spite of historically-high natural gas prices since the second half of 2021, Africa’s largest natural gas producer has been unable to materially grow export volumes in order to acquire more of the economic rents offered by global gas market balances.

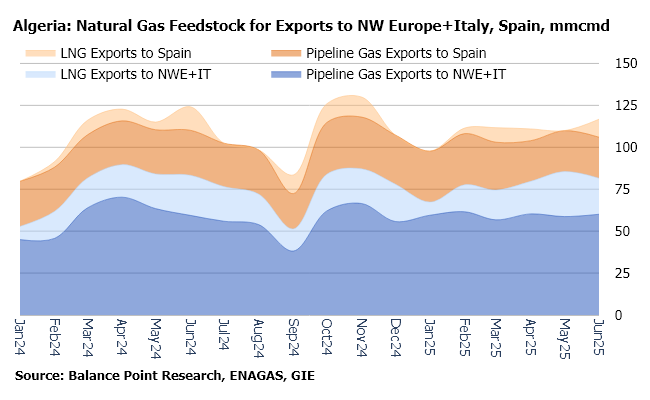

Data from the first half of 2025 tell a similar story. Natural gas feedstock for Algeria’s combined exports of natural gas and LNG to NW Europe, Italy and Spain remained range bound. Compared to 2024, they increased by just 1.4% year-on-year to 110 mmcmd (3.9 bcfd) in spite of an improved flat price environment for TTF and basis markets in Spain and Italy.

In part, the limited commercial ability of Algeria’s gas exports to capitalize on historic global gas prices is a function of its significant volume commitment to marketing exports via oil-indexed contracts both for pipeline and LNG exports. [Returning to the car analogy, this might be a similar choice to the no-thrills, continuously variable transmissions (CVT) on which many Nissan models now rely.] Based on theses contracts, the data illustrate some tactical, volume optimization of take-or-pay volumes by European buyers of Algeria’s pipeline contracts according to the price of oil, but relatively small-volume, opportunistic marketing by Algeria’s state-owned, natural gas marketing monopolist Sonatrach. There is also the issue of Algeria’s natural gas production getting diverted into its highly-subsidized downstream domestic gas and power sectors – a commercial dilemma that Sonatrach shares in common with other state-owned gas export monopolist companies located in countries that are similarly experiencing rapid population growth. Finally, Algeria’s upstream production has gas quality and reliability questions that challenge steady feedstock flow to all of its export channels.

A substantial round of under-construction, LNG export capacity particularly in the United States and Qatar is coming online during the coming months and years. Keen observers of the Atlantic Basin LNG market should keep a close eye on Algeria’s midstream and upstream gas sector to assess whether there could be a change in the steadiness of its underperformance. Of note, Sonatrach recently began construction associated with a US$2.3bn midstream investment targeting Algeria’s largest producing natural gas field, Hassi R’Mel. When completed, new midstream compression is supposed to help stabilize 188 mmcmd of existing natural gas production potential.