Global: LNG imports in the Iran conflict era

This week’s Iran conflict headlines have compelled Europe’s natural gas market to reprice expectations regarding improvement in LNG exports through the Strait of Hormuz. The TTF Sep26 contract is again testing the €50/MWh level after trading around a multi-week low of approximately €41/MWh just a few weeks ago in mid-June. While expectations for the Strait of Hormuz embroil the front of the TTF curve, further out the approach of incremental LNG supply from new capacity in North America becomes the heavier fundamental risk. Both the timeline and export rate uncertainty for these new sources LNG production will impact the back of the TTF curve for years to come.

A review of LNG import data from the second quarter of 2026 (2Q 2026) offers some insight for how the global LNG market might respond to a more elevated flat price level in the near term. Indeed, this week the front months of the TTF curve are trading at levels quite similar to the average outturn of 2Q 2026.

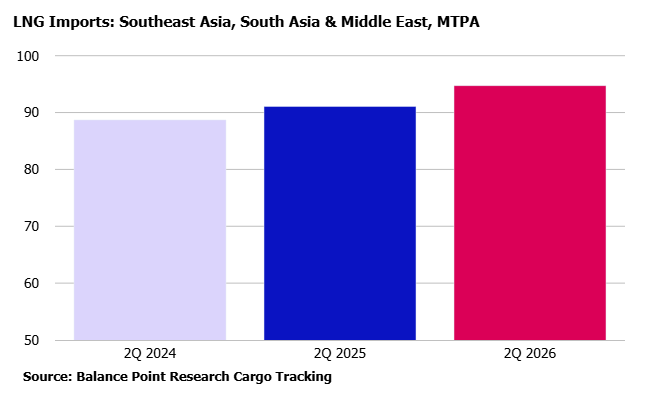

In Southeast Asia, South Asia and the Middle East, LNG imports actually increased year on year during 2Q 2026. The higher flat prices that prevailed this year did not deter key buyers. The strength of imports into India and Egypt in particular were critical to the region’s +4% year-on-year result.

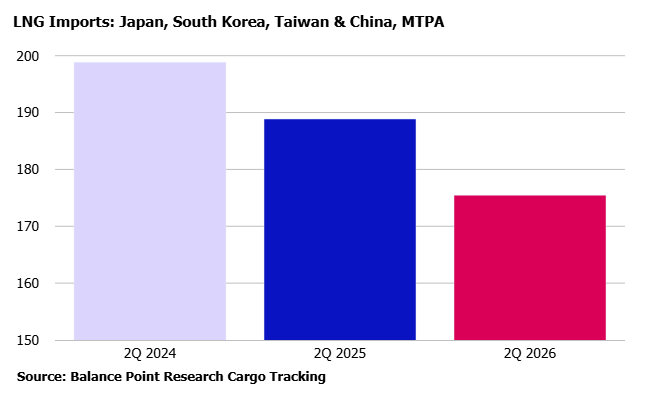

Northeast Asia supplied the largest volume of flexibility to the global LNG market. In 2026, imports in the second quarter decreased for the second consecutive year by -5% or more. The region’s country-level gas, power and LNG statistics highlight the degree to which its LNG-importing power markets continue to adjust their relationship with the physical LNG market compared three, five or 10 years ago. As the global LNG market returns to 500 MTPA and ultimately heads towards 600 MTPA based on the delivery of new liquefaction capacity, the power sectors of Japan, South Korea and China will emerge as a particularly dynamic space on which the global gas market is expected to physically solve with some regularity.

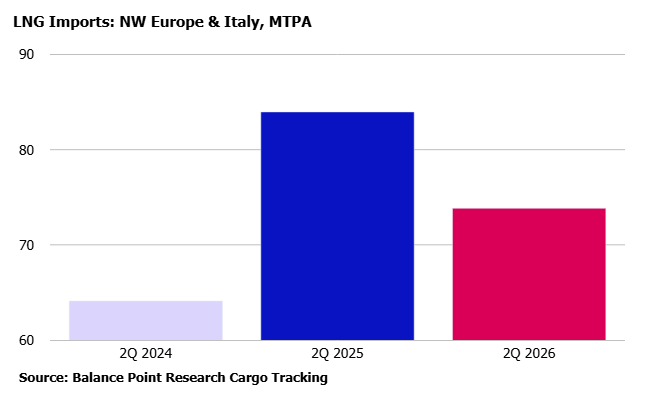

We conclude with the performance of LNG flows into the NW Europe + Italy import region. In the second quarter, imports declined by -12% year-on-year. While TTF flat price at forward curve for Aug26 through Oct26 is currently similar to 2Q 2026, this price level will not necessarily result in the same year-on-year arrival of LNG cargoes in the third quarter as it did in the second. Even if the situation for LNG supply from Persian Gulf exporters were to end up the same by volume, many other market dynamics in 3Q 2026 are expected to be different.