Taiwan: Nvidia’s JKM short

If expectations driving the market cap growth of US-listed semiconductor equities are correct, the demand runway for services and physical infrastructure related to artificial intelligence (AI) is immense. Putting stock prices aside, and returning to the realm of energy markets, the tightening impact of this financial juggernaut is already seeping into the margins of global LNG balances.

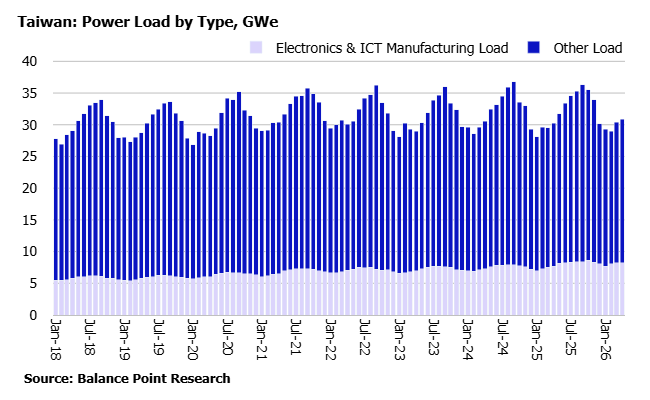

One of the clearest examples of the AI tightening trend in LNG markets is power load growth in Taiwan, which currently hosts the global economy’s most critical concentration of manufacturing for advanced chips, servers, memory and networking equipment. In the chart below, the collective power demand of this manufacturing activity is labeled as “Electronics & ICT Manufacturing Load”.

In 2026, for the first time, the sector’s annual share of Taiwan’s total power load is expected to surpass 25%. The timing of this growth event is commercially significant in light of the conflict in the Persian Gulf, and the continued outage of LNG exports from Qatar and UAE. Taiwan is not only importing more LNG in 2026, but the weighted average cost of its imports has significantly increased as it has been forced to replace lost LNG volume in the JKM-indexed spot market.

Weather conditions permitting, natural gas’ share of Taiwan’s power generation surpass 50% for the first time in 2026. The ongoing construction of new semiconductor fabs and other manufacturing supporting artificial intelligence growth will only continue, taking Taiwan’s LNG bid with it.