Japan: Demographic risk for LNG demand

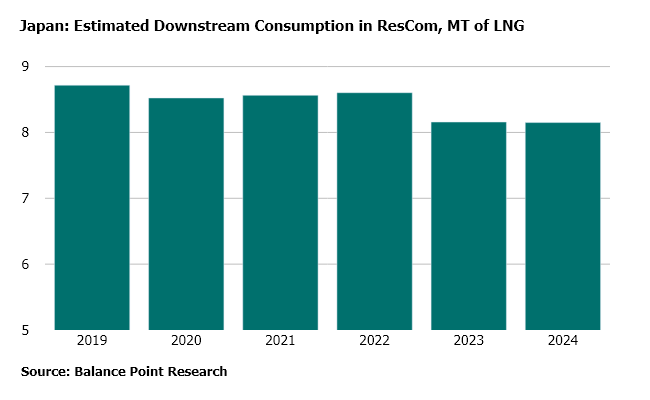

Japan’s consumption of LNG imports is in decline. From 2019 to 2024, imports fell by 10mtpa (-37 mmcmd, or -1.3 bcfd equivalent) owing to a multi-year, weakening trend in heating degree days (HDD) together with changes in Japan’s fuel mix for power generation.

Recently, a bullish buzz concerning data center investment for artificial intelligence in Japan has given life to a more optimistic outlook for Japan’s energy demand growth, and possibly for the trajectory of its LNG imports as well. For energy markets, such potential must be considered in conjunction with less bullish trends for energy demand. (The January 2025 DeepSeek model announcement destabilized the bullish case for the global AI industry’s energy demand outlook. The bulls also selectively ignore the possibility of AI models delivering low-cost, efficiency gains to legacy sources of energy demand.) Extremely relevant to Japan’s outlook is an emerging bearish risk factor posed by demographics.

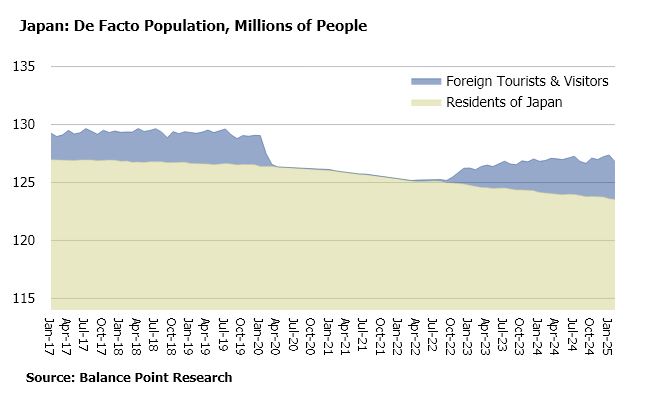

Between 2019 and early-2025, a weakness in birth rates coupled with restrictive immigration policy contributed a 3 million person decline in Japan’s resident population. Since its post-Covid reopening, Japan’s resident population has been declining by 50,000 people per month on average.

Although not representing full replacement value from an energy consumption perspective, it is still tempting to consider the numbers for foreign tourists and visitors as a temporary offset to Japan’s resident population decline rate. During the three months ending in February 2025, the average number of foreign tourists and visitors reached a historic high of 3.5 million per month. In January 2025, the monthly total of foreign visitors surpassed 3% of the resident population for the first time.

The overall decline in Japan’s resident population have also been offset by certain inefficient patterns. Between 2000 and 2020, the share of one-person households as a percentage of the total households grew from 27% to 38% according to census data. While older Japanese becoming the sole surviving member of a historically larger household has been one contributing factor, the concurrent trend of younger Japanese not getting married has also provided momentum. Given the bulge in the age distribution of Japan’s population for individuals currently in their late 70s, the negative impact of demographics on Japanese energy demand will soon reach a new gear.

For gas demand in the Residential and Commercial downstream sectors, temperature – not demographics – remained the dominant driver of demand during recent years. However, the available data for these sectors are starting to offer some warning signs for the emergence of alternative bearish drivers taking hold. Consider, for example, the perimeter of the Commercial sector as a function of the number of gas meters read for billing purposes. From 2019 to the end of 2024, the number of gas meters available to check declined by over 15,000. Such statistics give further support to the widely-reported Japanese economic trend of younger family members being unwilling to take over the family business from the older generation looking to retire. To better evaluate its future LNG bid, keen observers of Japan’s LNG market will need to grapple with Japan’s demographics, economy and demand for energy becoming increasingly intertwined.