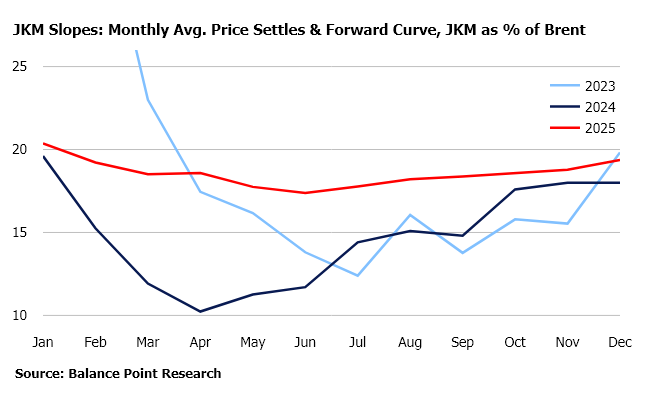

Prices: JKM slopes offer a note of caution

Since the Liberation Day announcements on US trade policy, JKM flat prices during 3Q25 and 4Q25 have fallen below the historical settles of recent years for multiple bullet months. While this might suggest that marginal buyers of LNG cargoes may now perceive LNG as cheap, from a different perspective LNG still remains expensive. JKM’s price relationship with crude oil, or slope value, remains elevated at forward curve compared to historical settles. Across 3Q25-4Q25, the average JKM slope is 18.5% compared to an outturn of 16.3% during the second half of 2024. At 18.5%, energy markets are pricing LNG more expensively than Brent crude on an energy equivalent basis. This was not the case for the majority of months in 2024.

JKM slopes offer a simple tool for evaluating the attractiveness of LNG compared to other fuel products offered by the global oil complex. Their elevated level at forward curve for the balance of 2025 remains a commercial challenge to the apparent “cheapness” of LNG flat price. During the weeks and months ahead, the relative differences in how global macro sentiment impacts trading in the crude and oil product markets compared to global natural gas markets will matter for marginal bids of LNG cargoes, in addition to the inter-regional flow of LNG cargoes in general.